Source: PaxForex Premium Analytics Portal, Fundamental Insight

Walmart recently announced that its stores would remain closed on Thanksgiving this year. That's the second year in a row, and the company became the second major retailer, after Target, to say it would not be open during the holiday.

Although stores were closed last year to contain the crowds during the COVID-19 pandemic, this may be the beginning of a trend that other retailers will follow. In fact, there may no longer be a reason for any of them to open on Thanksgiving.

Consumers doing their Christmas shopping are no longer limited to the four or five weeks between Thanksgiving and Christmas, but start shopping much earlier. Not just in early November - although, according to a 2019 RetailMeNot survey, 26% of consumers are shopping - but also in September (20%) and October (15%).

So retailers won't need to open on Thanksgiving as long as they have a solid platform to make online sales.

However, they will have to focus on product delivery as it will make a big difference in the consumer experience. While this bodes well for carriers such as UPS and FedEx, it also means that there will be less capacity available, leading to higher costs, and both carriers have already announced price increases averaging 5 percent.

But now that retailers have reopened stores, they can better leverage their in-store presence by using them as fulfillment centers. And to do so, they can copy the success of Walmart, which has long used its sprawling physical footprint to benefit from online shopping and in-store pickup.

While retailers will try to earn points by portraying generosity for letting employees stay home on the holiday, the real reason Walmart, Target, and other retailers can stay closed on Thanksgiving from now on is that they simply don't need to open.

Indeed, Walmart's online sales skyrocketed last year amid the pandemic, posting 69% (or higher) growth. Growth slowed to 37% in the first quarter, but that's still a strong performance considering there was a quarter behind with 74% growth and the start of the COVID-19 pandemic.

But Walmart could see a significant slowdown over the next few quarters, not only because the company is experiencing even stronger periods in the second and third quarters, but also because its biggest growth driver last year is now holding back growth.

When the pandemic hit the U.S. in March and April 2020, more consumers began shopping online in new categories such as groceries. According to eMarketer, online grocery sales in the U.S. grew 54% year over year in 2020. Walmart has been a major beneficiary of this growth after laying the groundwork for online grocery ordering from all of its stores in the previous few years.

However, Walmart and other online grocery vendors are having a hard time retaining customers. According to a report by Brick Meets Click and Mercatus, online grocery sales in May fell 16% year-over-year to $8 billion. It is also the second consecutive month of declining online grocery sales.

Online food sales in May were still well above pre-CoVID levels, and most of the pandemic's gains persist. However, they are no longer a source of growth for online retailers. In the first quarter of last year, about two-thirds of Walmart's online sales growth came from an increase in online grocery orders.

Not only is the online grocery sales market shrinking as we go through a period of challenging comparisons, but Walmart's market share is also shrinking as competitors quickly caught up with its position in grocery order fulfillment.

If these trends continue, Walmart's online sales growth rate could plummet by the end of the fiscal year 2022.

Last year, Walmart launched the Walmart+ program, the centerpiece of which is online grocery ordering. The $98 annual membership includes free shipping for online food orders, which normally costs $10 per order. It also includes free shipping on all Walmart.com orders, discounts on drugs and fuel.

Walmart, however, is struggling to keep subscribers to the new service. While unlimited free grocery delivery is the program's biggest and most advertised benefit, the company has had great success retaining customers who take advantage of fuel discounts, according to a Recode report. However, for most consumers, a $0.05 per gallon discount on fuel alone won't be worth $98 a year.

Walmart+ may continue to struggle as demand for online food delivery stabilizes and consumers get more opportunities to order supplies online.

In addition, there is also a domino effect. Walmart+ is expected to increase customer loyalty to Walmart.com. By increasing online food ordering, Walmart hoped to translate this into higher-margin sales of general merchandise through Walmart.com. So, not only does the largest category that provided growth in 2020 now act as a barrier to Walmart's continued growth, but it also potentially reduces sales growth for the entire e-commerce business.

Walmart still gets the vast majority of its sales from its physical stores, making it the largest retailer in the United States. But as more and more commerce moves online, the company will struggle to grow as fast as its competitors, and it will lose market share.

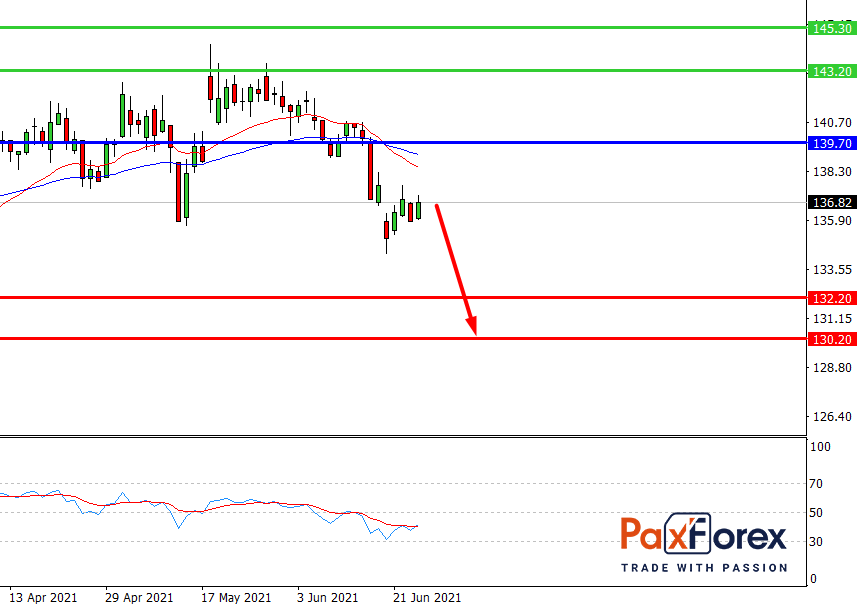

While the price is below 139.70, follow the recommendations below:

- Time frame: D1

- Recommendation: short position

- Entry point: 136.43

- Take Profit 1: 132.20

- Take Profit 2: 130.20

Alternative scenario:

If the level 139.70 is broken-out, follow the recommendations below:

- Time frame: D1

- Recommendation: long position

- Entry point: 139.70

- Take Profit 1: 143.20

- Take Profit 2: 145.30