Source: PaxForex Premium Analytics Portal, Fundamental Insight

Verizon Communications is having a great time in 2021. The company's second-quarter revenue rose an impressive 10.9% year-over-year, but given the negative impact of last year's pandemic, this growth was to be expected. Notably, Verizon also outperformed second-quarter 2019 by 5.3 percent, despite the continued negative impact of COVID-19.

Even so, the performance had little impact on the stock price, which hit a 52-week high of $61.95 last December but is currently trading around $55 per share. Does this create a buying opportunity, or is there cause for concern amid strong second-quarter results?

The second-quarter results point to a lot of positives in the company's direction. Revenue of $33.8 billion not only surpassed last year's $30.4 billion but also $32.1 billion in 2019. But even more significant is wireless revenue. It grew 47.7% year over year as more customers upgraded devices.

The growth in wireless revenue has been a long time coming. The advent of 5G technology promised new revenue opportunities, including upgrades to 5G-enabled devices. Verizon's latest quarterly results suggest this is happening.

Customer upgrades have resulted in about 20 percent of Verizon's wireless phone base now running on 5G-enabled devices. CFO Matt Ellis said he expects to see "good hardware volumes in the second half of the year" thanks to the company's promotions combined with new 5G-enabled devices hitting the market.

Verizon generated more wireless equipment revenue in the first half of 2021 than in the past two years.

The company's success in wireless revenue complements Verizon's consistency in wireless revenue. Revenue from this segment totaled $28.2 billion in the second quarter, surpassing 2020 ($26.7 billion) and 2019 ($27.4 billion).

Wireless revenue was driven by growth in the company's postpaid customer segment, the most valuable type of customer in the telecommunications industry. Net growth in postpaid customers increased to 528,000, surpassing last year's 352,000, and net growth in postpaid customers of 451,000 in 2019.

The company's strong performance in the first half of the year led Verizon to raise its 2021 total wireless revenue growth forecast to 3.5-4% from a low of 3%. Despite its success in the first half of the year, the company's stock price was little changed in the days following the release of its second-quarter reports. Several factors contributed to this.

Included in the quarterly wireless revenue was revenue from the Verizon Media division. This division includes Internet companies such as Yahoo! and it added $2.1 billion to the quarter's results, a 50 percent increase over last year. This result contributed to Verizon's service revenue and other segments compared to the previous year, but Verizon Media is selling out.

In addition, the company's debt rose. Earlier this year, Verizon had to spend $52.9 billion to get the critical spectrum needed to run its 5G network. At the end of the quarter, the company's total debt was $151.9 billion, up from $112.8 billion last year.

The debt load is a concern, but Verizon is reducing it. At the end of the first quarter, bthe total debt was $158.5 billion, so the company was able to write down $6.6 billion by the end of the second quarter.

In addition, Verizon's higher wireless revenue projections do not include Verizon Media's contributions. That's based on the strength of the wireless business, aided by factors such as growing customer adoption of more expensive data plans. In the second quarter, the company saw record growth in the number of new subscribers opting for unlimited premium plans.

We shouldn't forget about Verizon's dividend. Their payout is guaranteed thanks to the company's strong free cash flow, which totaled $11.7 billion in the first six months of 2021. $5.2 billion of that amount went to pay dividends.

Rival T-Mobile offers no dividend, and AT&T's dividend is likely to decline due to the impending sale of its media business. Meanwhile, Verizon has raised its dividend for 14 consecutive years and is expected to raise it again this year.

Verizon is well-positioned to deliver continued revenue growth as the rollout of 5G begins. The many positives in its business outweigh Verizon Media's increased debt burden and loss of revenue. These factors make the company worthy of investment, especially as a stable income stock.

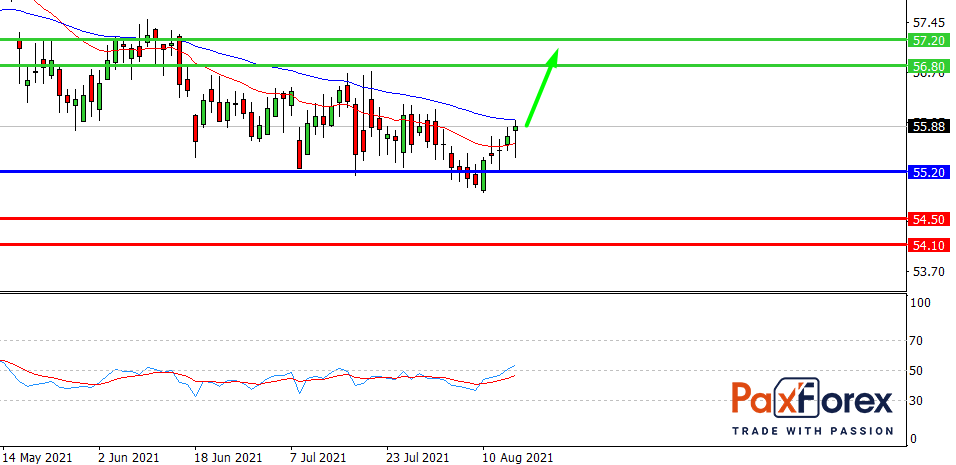

As long as the price is above 55.20, follow the recommendations below:

- Time frame: D1

- Recommendation: long position

- Entry point: 55.87

- Take profit 1: 56.80

- Take Profit 2: 57.20

Alternative scenario:

If the level of 55.20 is broken-down, follow the recommendations below:

- Time frame: D1

- Recommendation: short position

- Entry point: 55.20

- Take Profit 1: 54.50

- Take Profit 2: 54.10