Source: PaxForex Premium Analytics Portal, Fundamental Insight

HP stock has more than doubled in the past 12 months, recently hitting a record high in two decades.

This rally is a reflection of the modest rebound in the personal computer market before COVID-19 emerged, followed by a more rapid upturn spurred by the pandemic itself. As for the three-month stretch that ended in March, IDC's technology market survey found that PC shipments were up 55% year-over-year. Gartner estimates that figure to be closer to 32%, using slightly different criteria to define what constitutes a personal computer. IDC and another market research firm, Canalys, agree that PC sales will grow on average through 2025. All of this certainly bodes well for HP's business prospects.

However, there are a few points, largely ignored by the bullish rhetoric, that will work against HP stock sooner or later. If you're planning to get rid of the company's stock for the foreseeable future, now might be a good time. And if you've been thinking about getting into a long position, now is hardly a good time to do so.

HP, formerly known as Hewlett-Packard, certainly stands a good chance of presenting strong quarterly numbers next month. The analyst community predicts sales growth of nearly 16% -- according to IDC and Gartner calculations -- that will lead to a 72% increase in profits.

But in the current environment, it won't be easy to stick to that forecast.

IDC's expectations for cumulative annual PC sales growth of 2.5% between 2020 and 2025 include 2020 and 2021. These two tremendous years of growth outweigh the CAGR, which means that the last three years of this five-year period will be below average; they may even be negative. In addition, Canalys' cumulative growth expectation is 3.5% from 2021 to 2025.

An expectation of 8.4% growth between 2020 and 2021 means that the best growth is happening now or has already occurred.

The risk is that current shareholders underestimate how different the near future will be from the recent past. About two-thirds of this company's business is typically in the PC market, while a third is in the printer market, so the PC market is very important to the company.

However, investors should not blindly believe every analyst's estimate. Notably, however, the analyst community did not change its average target price of just under $31 when the stock was well above that mark five weeks ago.

Historically, the analyst community has reacted to changes in the stock's target price because these people use current information to make inferences about its future value. Only rarely has the HPQ price beat the consensus target, and when it has, not for long, and not by much. It is the longest and largest divergence we have seen above the average price target over the past two years. It is not usually the extreme that investors want to see.

This hesitancy to raise the consensus target is certainly not due to a lack of information, either. HP's first-quarter report, released in February, provided a clear earnings forecast for the second quarter, and IDC's long-term computer market forecast was released in January.

In addition, HP stock is now at a value level not seen since 2018. That's when sales and laptop prices were up, and shareholders were celebrating on the occasion of several small acquisitions. However, none of the tailwinds could last long, and as a result, the stock price quickly declined.

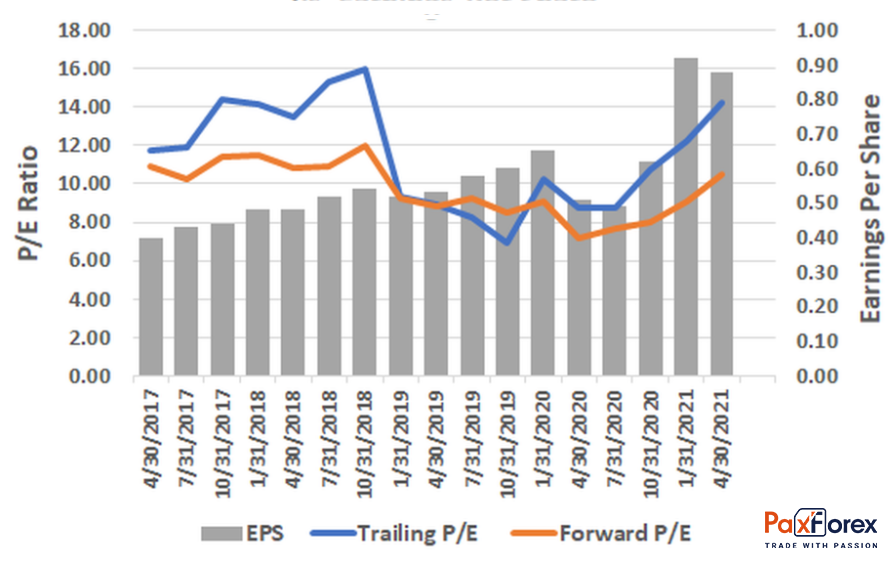

The chart below shows the company's outlook. The current 12-month price-to-earnings ratio is 14.2, while the projected ratio based on valuations is 10.5. That's cheap by technology stock standards, but not by HP's historical levels.

HP generally trades at single digits and about 7 in terms of predicted profits.

Don't get it wrong. In most cases, paying for a quality name is worth it in the long run... especially if there is sustained and significant growth. However, it's not obvious that HP has real growth ahead, which only increases the risk of a valuation that's already 20% above its 2019 and 2020 levels.

To be clear, many are more concerned about the stock than the company itself. HP may never be a high-growth company again, but it is a rare dividend asset in the tech sector for a certain set of investors. Even at its current high price, HP has a dividend yield of 2.3%, and the pressured operating income before COVID of $2.24 per share in 2019 easily covers an annual dividend payout of about $0.70. Well, there's always a small chance that the company will just find or develop a new market niche that will lead to unexpectedly strong growth.

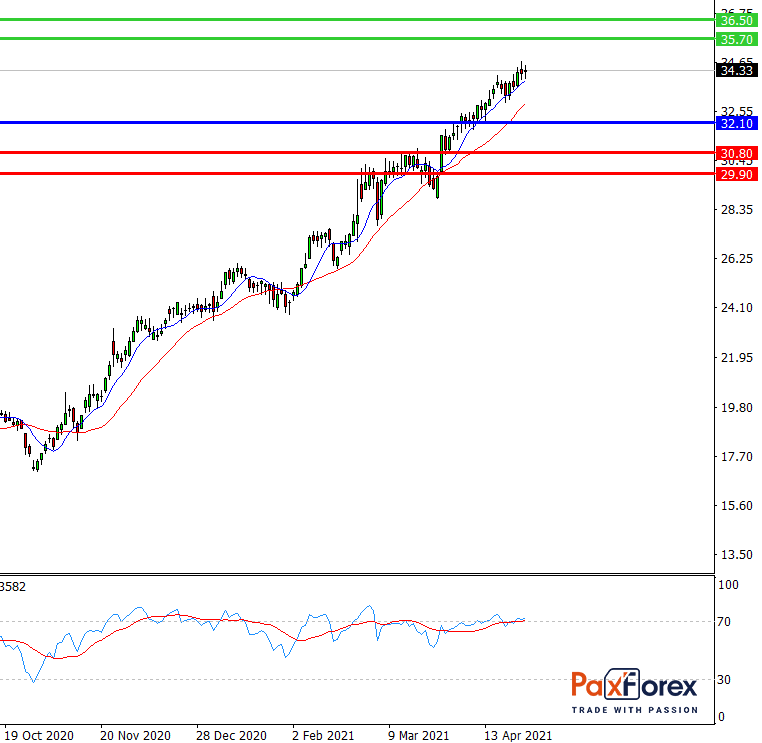

Provided that the price is above 32.10, follow these recommendations:

- Time frame: D1

- Recommendation: long position

- Entry point: 33.90

- Take Profit 1: 35.70

- Take Profit 2: 36.50

Alternative scenario:

In case of breakdown of the level 32.10, follow the recommendations below:

- Time frame: D1

- Recommendation: short position

- Entry point: 32.10

- Take Profit 1: 30.80

- Take Profit 2: 29.90