Source: PaxForex Premium Analytics Portal, Fundamental Insight

Alibaba is probably China's best-known technology business. It can boast of its biggest online marketplaces in the country, Taobao and Tmall, as well as the largest cloud infrastructure platform, Alibaba Cloud.

Alibaba went public in 2014 and became one of the fastest-growing companies for the next six years. The initial share price was $88 a share, trading started at $92.70, and hit an all-time high of $319.32 last autumn. After that, Alibaba has lost more than 30% of its value as it has continually made headlines for completely unpleasant reasons.

Let's take a look at why everyone is talking about Alibaba - and whether it can ever recover.

Much of Alibaba's decline can be attributed to antitrust litigation in China, which began last December and ended this April with a record RMB 18.23 billion ($2.82 billion) fine and new business restrictions. China's State Administration for Market Regulation (SAMR) started the investigation in reply to criticisms about Alibaba's exclusive deals with big brands that banned them from listing their products on competing online shopping sites.

Alibaba paid a fine equivalent to 2.5% of revenue and 12.1% of net income in the fiscal year 2021, in the Q4 of this year. The fine alone will not have a significant influence on Alibaba's long-term growth.

However, SAMR also forced Alibaba to terminate exclusive deals and imposed additional fines on the company for earlier declined acquisitions. Those fines were much smaller, just ¥500,000 ($77,224) per violation, but they could block Alibaba from developing its retail and cloud ecosystem with new acquisitions in the future.

These new restrictions could make it easier for smaller e-commerce rivals such as JD.com and Pinduoduo to divert customers from Alibaba's shopping sites. They could also give smaller cloud infrastructure competitors, including Huawei, Tencent, and Baidu, a chance to catch up.

Challenging Alibaba's established e-commerce and cloud business remains difficult, but these uncertainties cast doubt on analysts' expectations for sales growth of 30 percent this year.

Other storm clouds have hung over Alibaba: the sudden disappearance of its co-founder Jack Ma and the unpredictable prospect of his fintech company Ant Group.

Ma hasn't been CEO of Alibaba since 2013, and he stepped down as director two years ago. Nevertheless, Ma is still regarded as the face of Alibaba and is more recognizable than its current CEO, Daniel Zhang.

So when Ma infuriated the Chinese government by reprimanding the country's banking system last October, the outcomes troubled Alibaba. In response, the government suspended Ant's IPO in November, dashing Alibaba's hopes of profiting from Ma's 33% stake in the company.

The government has also offered to regulate Ant Group's Alipay and Tencent's WeChat Pay, which have a near duopoly in the Chinese online payments market, as financial institutions.

These new restrictions could stop Alibaba and Tencent from utilizing their affiliated payment platforms to tie retailers and other businesses to their sprawling ecosystems.

By themselves, the actions against Ma and Ant will not cause Alibaba to collapse. But together with the antitrust investigation and new business restrictions, they show that the Chinese government intends to limit Alibaba's long-term increase.

Many U.S. investors did not approve of China's actions against Jack Ma, but Charlie Munger, a celebrity investor who purchased a large stake in Alibaba through the Daily Journal earlier this year, recently expressed the opposite view.

In an interview with CNBC, Munger called Ma "arrogant" and said that "the Communists did the right thing" in curbing him. These controversial comments could make it difficult for U.S. investors, who do not share Munger's enthusiasm for Chinese law, to buy Alibaba stock.

At the end of 2020, the U.S. passed a law that would delist stocks of foreign companies that fail to comply with stricter auditing standards within the next three years. These businesses will also have to prove that they are not owned or controlled by a foreign government.

Alibaba, JD, Baidu, and many other Chinese technology companies have already held secondary IPOs in Hong Kong in response to these threats, a strong indication that they will not comply with the new U.S. auditing standards.

China also plans to crack down on the VIE (variable interest entity) model, which has allowed its leading tech companies to circumvent restrictions on foreign investment in sensitive sectors. VIEs are holding companies based in intermediary countries, such as the Cayman Islands, that list their shares on U.S. exchanges.

If China closes this so-called loophole, most Chinese companies will no longer be able to list on U.S. exchanges. Those that remain, such as Alibaba, would seem to be trading in turbulent times.

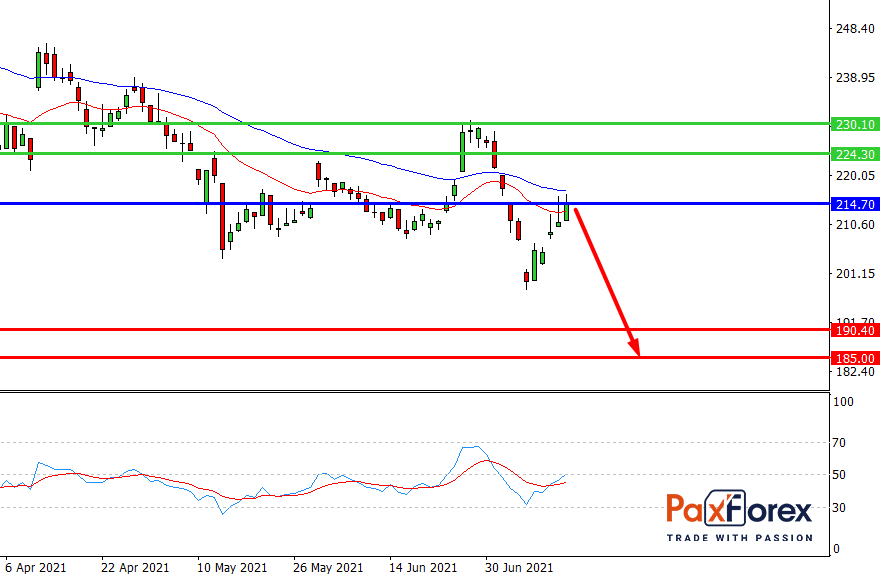

While the price is below 214.70, follow the recommendations below:

- Time frame: D1

- Recommendation: short position

- Entry point: 206.00

- Take Profit 1: 190.40

- Take Profit 2: 185.00

Alternative scenario:

If the level 214.70 is broken-out, follow the recommendations below:

- Time frame: D1

- Recommendation: long position

- Entry point: 214.70

- Take Profit 1: 224.30

- Take Profit 2: 230.10